Update Post on $INDV, $CDLX and $MYPS

A homerun, a single and a balk

Dear subscribers,

I wanted to post a quick update to the 500 Hours Project. I have had to delay publishing the next few rounds of ideas due to some professional conflicts. However, I have two new ideas tee’d up which I hope to publish within the next month as well as some general investing/career stuff.

However, I first wanted to catch up on the first three published ideas as I strongly believe that money is made during the hold period, not the buy side decision:

Idea #1 - Indivior ($INDV)

+67% since publication versus S&P500 +6%

The core thesis of INDV continues to play out. While the stock has increased in price, I actually believe that risk/reward has improved. There are three reasons for this:

A) Lower Risk - Higher than expected cash flows should enable INDV to internally fund its legal liabilities, debt payback, drug pipeline capex and share buyback. FCF is higher from Subutex more slowly ceding market share to generics and Sublocade is approaching FCF breakeven as sales ramp.

B) Re-rate of valuation to a Going Concern - INDV appears to be reinvesting into a viable drug pipeline and long-term strategic growth plan. This would re-rate valuation and given INDV a terminal value instead of it currently trading at essentially DCF runoff value. Building out INDV’s pipeline would also improve valuation under an M&A scenario as pharma acquirors place higher premiums on platforms that can handle larger growth capital investments.

INDV trades at 2x revenues versus peers Alkermes and Camerus at 5x and 11x.

C) Downside protection from Share Buyback – Indivior executed $31M in share buybacks out of $100M authorized in roughly one quarter. The company was aggressively buying in the $1.75/share range which provides a bit of a soft floor.

To reiterate again, going forward, it will be critical for investors to pay attention to two items, Sublocade OHS penetration and Fentanyl abuse:

1) Key KPI is OHS penetration and volumes

Only +300 activations out of +500 priority organizations but only 5% incarcerated patients are currently receiving treatment. Sublocade growth is in inning 1 or 2.

2) Fentanyl entering the investor’s lexicon

One of the more differentiated views of the original INDV thesis was that Fentanyl would drive higher opioid addiction and abuse. In the recently reported quarter, INDV updated its label for Fentanyl abuse and remarked:

“I think the Fentanyl claim, obviously, is quite pertinent given what is happening with overdoses. With overdoses over 70,000 a year and about 75-ish percent of those the data says are synthetic opioids, fentanyl and other types. So, it is quite pertinent. It is a buprenorphine-based claim, not a SUBLOCADE claim, but we think it is quite pertinent. And listen, we think it's created some discussions within the medical community with regards to broadened use of buprenorphine and SUBLOCADE, which is a buprenorphine product to address this.”

Idea #2 - Cardlytics ($CDLX)

Airgap 2Q and 3Q behind us, and setup into 2022 compelling

Back in August, CDLX’s 2Q21 earnings were ROUGH as expected -its stock declined >20%.

However, CDLX reported its 3Q21 results earlier this week and it showcased some momentum in its longer-term growth drivers. The “air gap” in fundamentals from CDLX’s transition is entering into its later stages.

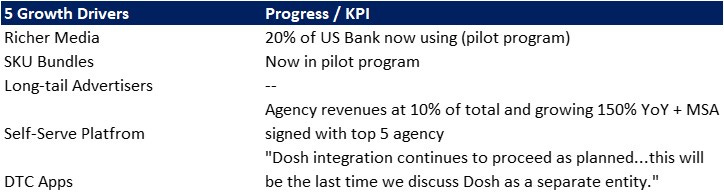

There actually isn’t too much to update on the original thesis, but the following are interesting KPIs to monitor on the 5 growth drivers from CDLX’s 3Q21 earnings.

As you can see by the chart above, CDLX is still in transition mode. Each growth driver is progressing at a different pace, but I expect demonstrable translation into ARPU and earnings from these catalysts in 2022.

I continue to conduct interviews with agencies, advertisers and customers for updates on progress. From these channel checks, I believe that most of the pilot programs are trending a bit better/faster than what management communicates to investors on its calls.

The standout item from the past two quarters is that pricing (ARPU) is finally trending the right way (though far from great tbh). ARPU was up 24% YoY (or roughly 26% on a same store MAU-adjusted basis) which is great, however, it it still well below CDLX’s 2018 ARPU numbers in the mid $2 range which I view as its natural yield level. That said, growth was a bit more impressive considering that its highest margin business, Travel, remains under pressure YoY and much lower versus pre-pandemic levels.

While 4Q21 earnings will likely still not showcase CDLX’s potential either, I continue to believe that the setup into 2022 is compelling and catalyst rich.

Idea #3 - Playstudios ($MYPS)

This idea was a short-term trade that ultimately was not taken. IDFA and ATT headwinds are starting to bite hard, which is increasing user acquisition costs. This puts pressure on newly launched games which does not bode well for the lynchpin of MYPS’ story - Kingdom Boss. The launch of Kingdom Boss was delayed until later this year.

I still think its worth following MYPS given its huge liquidity position (~$300m) and potential growth of Kingdom Boss and inexpensive valuation (enterprise value of $362M). However, I personally (greedily) would like to make an investment in this stock at current valuation AFTER user growth has stabilized and Kingdom Boss has successfully launched, which may not happen. I also just do not want to own shares ahead of the PIPE/SPAC lockup expiration next June.

Thanks for reading and hope to bring some fresh content shortly - as always feel free too reach out for discussion!

Best,

A Man In a Basement

Stockdweller@gmail.com