First Post of 500 Hours Project! - Indivior ($INDV)

Indivior (INDV): The Pepsi of Opioid treatment, catalyst rich w/ >150% upside

Executive Summary

Life-saving, injectable treatment for opioid abuse

Exponential demand for opioid treatment driven by Fentanyl scourge

Becoming a standardized tool in large organized healthcare systems

Current valuation ‘hangover’ should end soon - drama with former management (ousted) and lawsuits (resolved)

Improved governance, board and management - committed activist (Scopia)

Injectable ‘depot’ technology is 1st to market; superior product-market fit

Growth story is uncorrelated to the economy

Stock priced for less than runoff value and <5x peak EBITDA in base case

Expect Strategic Review (sale) shortly if public market discount persists

BUY THE LONDON OTC LISTED STOCK, NOT THE US LISTED ADR!

Why can’t large institutional asset managers own this?

Part I) Competitive Advantage

Superior product market fit and first mover in growing addiction market

Indivior was spun out of Reckitt Benckiser (RBGPF) in 2014 to better capitalize growth for its primary assets - Sublocade (injectable depot) and Suboxone (oral film) - which treat opioid addiction.

These drugs are already FDA approved and are very well known in addiction circles.

Sublocade (injectable) treatment is the crown jewel asset for the investment case.

Currently, the only FDA approved injectable depot treatment available.

Once-monthly injection Sublocade’s depot automatically dispenses medication and dissolves. It cannot be tampered with as dose is placed in abdominal fat.

The acting ‘agonist’ reduces cravings and the chance of overdose.

Strongest product-market fit for opioid abusers who are most at risk and unreliable to adhere to a schedule of treatment. Sublocade offers:

1) Increased patient adherence

2) Lowers diversion risk (re-selling on the street)

3) Longer-lasting treatment that prevents overdoses

These are all significant concerns in the healthcare/law enforcement communities

Why take medication at all?

Unfortunately for these poor souls, Medication-Assisted-Treatment is typically their only shot at recovery. Generally speaking, recovery chances increase ~2x with meds and the ability to socially function is also improved.

Opioid Use Disorder (“OUD”) Market Size

3M million US citizens and 16 million worldwide(1) currently suffer from OUD.

Indivior targets a modest Sublocade peak patient penetration of 183,000/year (or 6% of users), from 29,000/year run-rate currently (or 1% of users).

The OUD patient population is growing from:

Fentanyl use increasing – A street drug whose growth is heartbreakingly high and overwhelming the system even as prescription opioids tail off…

“I don’t think the general public really understands the scope of the epidemic,” said Franco. “If you look in individual counties’ data and in all of 2020, 3 times more people died in San Francisco [of drug overdoses] than they died of COVID.”

Covid has worsened Opioid/Fentanyl abuse

https://www.ama-assn.org/system/files/2020-12/issue-brief-increases-in-opioid-related-overdose.pdf

What is a realistic market share target for Sublocade?

Product-market fit is strongest for those who struggle with adherence and diversion

Winning 5%-10% of the most severely addicted seems like a conservative baseline market share assumption

Additional penetration for Sublocade in criminal justice system?

“we continue to prepare for easing of COVID to re-enable engagement with the criminal justice system. Data indicates that 65% of OUD patients flow through the criminal justice system at one point or another during their patient journey.”

-Indivior 1Q21 earnings

3M U.S. OUD patient population x 65% flowing through criminal justice system = ~2M patients where Sublocade has the strongest product-market fit

Sublocade has tremendous potential to save lives within the incarcerated and recently released populations (Vera article)…

“A seminal study in Washington State found that, in the two weeks following their release, people who had been incarcerated in state prisons were 129 times more likely to die from an overdose compared to the general public.”

Sublocade is the best positioned drug to save lives as it is the longest acting (~1 month) medication and adherence/diversion risks eliminated!

Patient churn - this is morbid – but is a real factor. If overdose deaths are reduced, then patient pool for Sublocade likely increases.

~70k patients die each year from overdose (38% of Sublocade’s target peak sales).

Elongating treatments - Many patients are not churning off the medication. Buprenorphine treatment programs can last for years

In sum, these four factors could enable Sublocade to reach 10-15% market share or approximately 2-3x Indivior’s peak target.

Competition

Camurus (CAMX) has a competing ‘depot’ product called Brixaldi that will potentially be approved by the FDA by December 15.

Brixaldi has been delayed due to manufacturing issues from its oil-based depot

If approved, Brixaldi offers more customizable doses than Sublocade on a more frequent basis (weekly injections).

Brixaldi will certainly compete with Sublocade for a large and growing market, however, it appears that it is a better fit for outpatient clinics and less severe addiction cases i.e. those that can be relied upon to show up for consecutive, multiple treatments.

Part III) Why is the stock discounted?

The Indivior Soap Opera (2014-2020)

Shortly after the spin from Reckitt, then CEO Shaun Thaxter, led the company astray. You can read tons about the prior situation (here is the indictment).

Long story short, Indivior stock crashed and has failed to recover to pre-scandal highs

However, in the past 9 months Indivior has cleaned up its act:

Settled lawsuits that posed existential threats: DOJ, States and Reckitt

Revamped mgmt. and board and signed shareholder agreement with Scopia Capital

Indivior’s board fumbled over trying to payout its criminal CEO and then it recently cleaned up this part of the board too with a succession plan – yea, wow.

In sum, Indivior went through A LOT.

However, Sublocade continues to show promise as strong potential blockbuster drug (>$1bn in peak sales).

If Sublocade growth targets are hit, stock would likely increase substantially. However, the market is currently pricing in heavy discounts from:

1. Drama hangover

2. BS perceived as (slightly) undercapitalized to support Sublocade growth

3. Slower Sublocade script growth – this is set to change, see section below

Part IV) What could close the gap to intrinsic value?

Sublocade scripts/revenues/cash flow can trend higher from:

1) Improved patient access

In-person treatment facilities still reopening from Covid-19.

Only operating at 50%-60% of capacity in 1Q21, hampering Sublocade’s growth. Weekly scripts approaching 1,600/week up +40% from ~1,100 during corona.

Newly issued (April) guidelines by Biden administration enables faster treatment, removes red tape.

2) Fentanyl increasing the patient pool (wouldn’t take the under on this)

3) Ramping penetration in Organized Health System (“OHS” e.g. jails, VA, etc)

Federal sales programs established (hardest part), now scaling (easier part)

“In Q1, we activated 22 new parent organized health systems, bringing our total count to approximately 230 against our 500-plus goal. This channel now accounts for over 40% of SUBLOCADE net revenue exiting Q1 and over 70% of our growth.”

-Indivior 1Q21 earnings

4) Competitor drug delays (described above – still faces FDA approval)

5) New leadership making tough, but shareholder friendly decisions e.g. cut opex

Part V) Risk and Reward Scenarios

Tons of variability here! – be conservative

Four primary valuation considerations:

1. Sublocade (growth asset): can it hit $1bn ‘Blockbuster’ target?

2. Suboxone (high cash flowing, but wasting asset): this is off patent protection, how long will cash flows last before generics takeover market share?

3. Perseris (pipeline asset): approved schizophrenia drug with $20M in revenues in a $200M - $300M TAM market

4. Platform IP + operating infrastructure

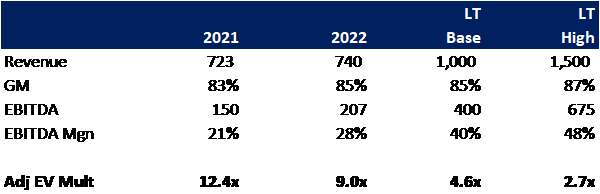

Let’s consider #1 (Sublocade) first:

Projections below are borrowed from a VIC writeup in December 2020 – so far, Sublocade is trending in line with these projections

Sublocade NPV alone likely worth $2bn-$2.8bn or +20%-50% upside alone

#2 – Suboxone (opioid treatment film)

Suboxone is off-patent and its market share is being eroded by generic competitors.

However, market share loss has been slower than expected for numerous reasons e.g. state sponsored payers mandating labeled drugs and won’t use generics

Indivior recently raised Suboxone guidance even with generics ramping

Run-rate revenues of ~$450M but declining

Margins/cash flows running higher, offsetting negative margin mix from Sublocade as ramps

Capitalize conservatively!

$350M - $750M? (20% - 40% of current enterprise value)

#3 (Perseris/drug pipeline) and #4 (platform IP)

Hardest to value

$300M?

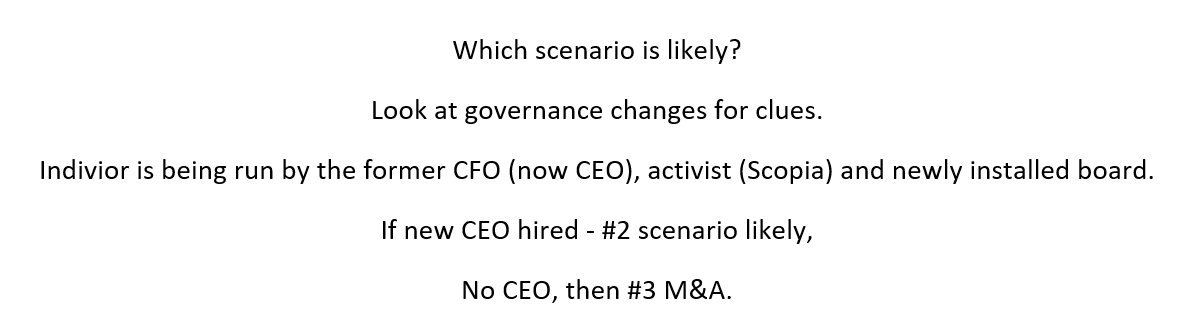

Consider two (more realistic) scenarios:

1) ‘Going concern’ - cash flows reinvested into adjacent addiction treatment markets

Cocaine addiction? Smaller TAM than opioids but would stabilize long-term cash flows and reinstall a going concern/terminal valuation

Sublocade to +$1bn

10%-12% WACC

Modest terminal value

NPV >150% versus current stock price

2) M&A Sale: >250%?

+3x revenue multiples (large pharma can strip out ~40% of opex and pay up)

M&A premiums rising!

2x, 3x, 4x?

Part VI) Additional resources

1) Biden’s Opioid plan – tons of details (MAT sections most relevant)

https://joebiden.com/opioidcrisis/

2) Detailed backstory on opioid use disorder and treatment plans in jails

https://mcrh.msu.edu/resources/mat_in_jails_prisons_toolkit_final_2020-01-30.pdf

4) How New Hampshire and Hawaii are taking on MAT stigma with jail pilot programs:

https://www.nhbar.org/expansion-of-drug-treatment-services-for-inmates/

5) Queensland study comparing Sublocade and Brixaldi (interesting data page 43)

https://www.health.qld.gov.au/__data/assets/pdf_file/0032/932684/lai-bpn-clinical-guidelines.pdf

6) Patient level Sublocade descriptions (“Cons” section highlights extended usage / elongated use cases)

https://opiateaddictionsupport.com/sublocade-reviews/#Sublocade_8211_Review_of_Pros_and_Cons

7) California Opioid plan for jails (most comprehensive in nation)

https://www.latimes.com/california/story/2021-06-07/opioid-overdoses-sheriff-narcan-jails

Fantastic body of work on this. Thanks for sharing.

Two main questions:

1) What will make Sublocade the preferred choice vs. the monthly version of Brixadi?

The Australian usage guide you linked to suggests that the weekly Buvidal (Brixadi's brand name in that market) can be used to fine-tune dosage before moving on to a monthly shot. So this is actually an advantage vs. Sublocade, but it's an *optional* advantage, i.e. if the practitioner and/or patient sees a reliability risk then they can go straight to the Buvidal (or Sublocade) monthly shot to mitigate the patient's ability to change their mind or make a bad decision (relapse) later.

Your arguments (and reading a bunch of the patient posts in one of your links above) convinced me of the value of a monthly shot as a superior way to do MAT. So I'd guess that there's enough market for two competitors, but pricing/margins then come into question. Do you have any data on market share/pricing in other countries where the two compete head-to-head? I suppose to the degree that governments are the primary/only payor that this may or may not be helpful for calibrating expectations in the US.

You mentioned Sublocade having first-mover advantage; is that advantage demonstrable in similar scenarios (i.e. a second highly effective medicine comes on the market to compete with the first)? Any lessons from what happened to market share/pricing?

2) Intent to maximize Sublocade/run off/sell vs. maintaining going concern status.

You touched on this quite a bit. I think your take is reasonable but I'm not sure how to read the tea leaves apart from that.

For instance, the below article mentions Indivior pursuing a cannabis addiction medication, and that Indivior could own the molecule's IP owner up to $100mm for certain milestones. I'm guessing those milestones are akin to full commercialization of a drug, but do you take this as them keeping their options open, or a clear sign they're looking to keep functioning as a going concern?

https://www.drugdiscoverytrends.com/indivior-eyes-cannabis-disorder-treatment/

Has Scopia stated its ideal direction for the company?

Also along these lines, the recently announced buy-backs are great in the sense of shareholder returns but they do nothing to beef up the balance sheet. I don't have any concept of what it would cost to ramp Sublocade all the way to $1B but already returning capital to shareholders seems like the move of a company that wants to focus on what they already have. I know many companies want/try to do both and maybe at 85% gross margins they can. So I don't have an opinion here as to how to interpret the buy backs but would be interested in your take.

Thanks again for sharing.

I really like your approach; it occurred to me that one of my biggest successes in a stock pick was due in large part to the fact that it wasn't investable by institutions (tiny float). This later changed and I was fortunate to participate in a massive upward re-rating.

Given where broad valuations are, I believe that one has to selectively pick from the "market of stocks" rather than just own the stock market in order to be very successful.

I'm looking forward to digging into your second article in the near-future.