Stuck in the Middle with (Rok)U

Part 1 of a 3 Part Series on $ROKU

This is a hard thesis.

With this blog, I am not aiming to do a comprehensive basic pitch, but rather to give readers a more specific and in depth investment angle. As such, if you are not familiar with the basics of Roku then this article may not be the best first read.

Given the length and complexity of this writeup, I have broken it into three parts:

Part I) Summary

Part II) Sector focused – Roku’s AdTech advantages that underwrite FCF growth

Part III) Roku’s De-Risking Content Pivot and Valuation

Recommended Reading

Overview of Roku Biz Model by Fundasy

Investor Presentation

Part I) Stuck in the Middle with (Rok)U

I invest in a lot of AdTech companies. I am attracted to the sector because there is a tremendous amount of money in motion and a lot of innovative, hypergrowth business models. While I don’t always get it right, these sector characteristics make for great investing over the long-term.

While I am a generalist, over time it is possible to hone in on sector pattern recognition. This is what attracts me to Roku’s stock right now. Essentially my core thesis is that the market is underappreciating the power of Roku’s Programmatic ad platform to generate FCF as well as its de-risking effects on Roku’s future business model.

I see a disconnect between Advertising industry pundits and investors. Investors seem to underappreciate the nuances of CTV AdTech supply chains which are not commodified like linear TV. Roku has tremendous advantages in CTV AdTech which will be discussed in more detail in Part II.

While Roku would get demolished if it had to compete head-to-head with Megacap buzzsaws like $AMZN and $GOOG in a commoditized business, I see CTV AdTech as getting much richer, complex, custom, integrated with E-Commerce and therefore much, much harder. Under these pretenses, I believe that the future competitive landscape in CTV will offer a more even playing field for Roku to compete. This is seemingly in striking contrast to the bearish chatter on terminal value risks that have contributed to valuation falling ~70% (ofc I acknowledge macro has been tough on growth too).

CTV Market Shifts are Moving in Roku’s Favor FAST

Roku has a dominate position in a subsector of the streaming space; Free-Ad-Supported-TV or (“FAST”). Roku “distributes” 3rd party FAST content through its TV OS platform. It also takes ownership economics in FAST content through licensing partnerships and creating its owned original content. FAST viewership is taking share in the US, and it is the dominant form of consuming TV streaming abroad.

Consumers are price sensitive in paying for streaming content, so FAST provides the consumer with another form of payment – time (watching ads).

FAST content is funded through advertising, but specifically a certain type called Programmatic. As we will explore in detail, Roku dominates CTV Programmatic marketshare as it wins roughly 50% of the pie. I believe Roku is set to continue dominating CTV Programmatic advertising for at least the next three or so years.

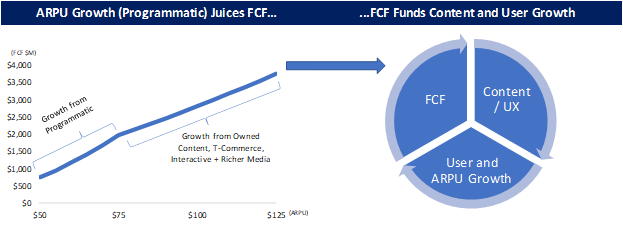

Roku’s Programmatic Growth Translates to Higher FCF Conversion than Street

Finally, if the above holds, I believe that the Street is significantly under-estimating the margin potential of Roku and subsequently its FCF conversion. From 2022 to 2025, Consensus is modeling only 700 bps of EBITDA improvement, from 14% to 21%. However, as I will discuss in more detail in Part III, Roku’s Programmatic growth is a much higher incremental margin than its core business. There is little incremental corporate cost structure as Programmatic scales given it is an automated ad exchange and is handled by 300 or so employees.

Programmatic FCF Generation Will Fuel Roku’s De-Risking Pivot

Most importantly, with Roku scaling FCF through its Programmatic division, it can build out an improved Content and UX strategy. Roku likely needs to invest in original CTV content and viewer UX in order to more compeitively position its value proposition to the consumer.

This reflexive FCF, User and Content flywheel is what will ensure the success of Roku’s long-term strategy – to entrench itself as the mesh-point between CTV and the living room.

Managing this mesh-point between users and their TVs is getting more complex as effective CTV AdTech execution will require making the relationship between users and TV a two-way street. Users will share an increasing amount of data and interaction with their televisions in order to improve UX (more targeted and fewer ads, content discovery, app access and payments, etc.). CTV platforms will need to marry this user data into much more effective and efficient advertising. Its hard to envision a future where untargeted linear TV advertising effectively competes against targeted, data driven and user-centric CTV ads.

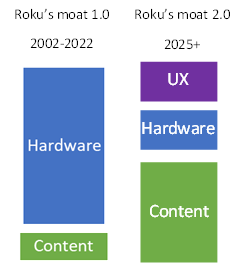

Roku’s relationship with the TV consumer is changing. If it can execute the pivot from being a “better remote” to a “better remote + Content + UX” it will have a much more entrenched, profitable, durable and valuable business.

Roku’s execution risk is extraordinarily high, but so is the potential reward as inflecting FCF with a simultaneously de-risking business model is multi-bagger material.

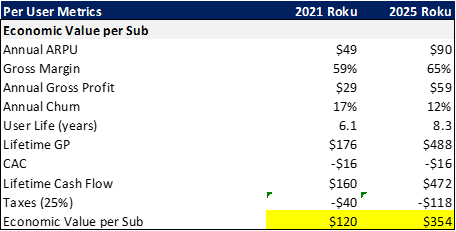

As I will detail further in Part III, Roku’s valuation is challenging to approach given the variability in viewpoints of its terminal value and risk premia of its cash flows. I prefer to take a user-centric valuation approach. As the chart below highlights, I believe that the value per subscriber that Roku captures is set to triple in the next three or so years.

In Part III, I will showcase how I believe this inflection in user value could translate to compelling IRRs on Roku between 20%-50% per annum.

Thank you for reading!

I appreciate any support through sharing or forwarding!

-A Man in A Basement

Amazing work....

I wonder what his thoughts are on the company now.