Roku’s FAST Cash Flow

Part II of III

Part II) Roku’s FAST Cash Flow

Programmatic CTV supply chains are a mess. Therein lies the opportunity for Roku to continue capitalizing on its market lead and scale FCF. This is Part II of III on my Roku investment thesis. This writeup will focus on Roku’s competitiveness in the CTV advertising sector.

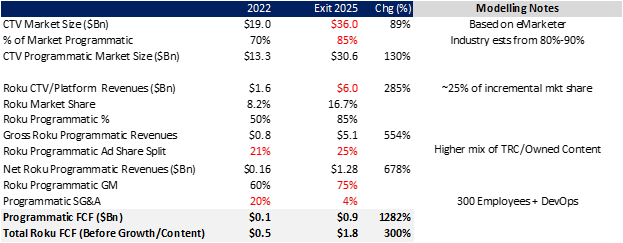

As you may recall from Part I, Roku’s programmatic advertising revenues are the critical assumption in my above Street free cash flow forecast.

These free cash flows will underwrite a pivot in business model towards more original content for Roku which I will discuss in the final part of this Roku trilogy.

Please note that Substack is limited on the memory of these writeups, so I have posted a PDF with the full text separately which may be more conveinent to read. I have posted as much as I could of the writeup below as well

Roku Best Positioned to Capture Streaming Paradigm Shift from Subscriptions to FAST

Roku is already the #1 OS platform used to stream content in the US. It has a commanding lead in viewership time (chart below) which is a superior KPI in monetizing FAST content (versus OS device footprint).

Source

Historically, TV OS manufacturers like Roku primarily competed on offering the viewer a more intuitive remote and (relatively) simplistic software to navigate multiple streaming apps. Competitor TV OEMs (Samsung, Vizio) were slow to react in creating an organized User Experience (“UX”) solution. This created an opening for Roku who was able to build a solid brand and capture the TV OS device lead in the U.S.

That said, one of the emerging risks for Roku is that TV OEMs and Google products are getting more competitive. As you can also see in the chart above, this risk is real as Samsung took 3 pts of market share, LG took 2 pt, and Android took 1 pt, though these gains seemed to disproportionately come from AMZN’s market share (down 3 pts vs Roku losing 1 pt). TVs are replaced every 8 years or so, which means that even if Roku’s competition heats up considerably, its lead in user base will still be sticky for a few years.

However, competing on hardware is yesterday’s game. Going forward, there is a paradigm shift in how consumers are streaming content. Previously, streaming was dominated by pay subscriptions apps like Netflix and Disney. Now, Free-Ad-Supported-TV (“FAST”) video consumption has overtaken Subscription-based.

Why?

Demand for TV content is insatiable. But the consumers ability to pay is limited. The #1 search term on Roku devices is “free” aka FAST. As the survey below highlights, price is the number one consideration for video streaming attributes.

Internationally, FAST is even better positioned. As you can see, it is projected to become a much larger piece of the streaming pie, particularly as international consumers are more price sensitive when it comes to paying for CTV. They much prefer to pay with time over cash!

“FAST platforms will expand globally and will represent 80% of the CTV growth. To offer more consistent data on CTV, audience and measurement platforms will increase their efforts in this direction.”

Penelope Lima, senior director - global supply strategy, VDX.tv

Programmatic is the Lifeblood of FAST

Linear TV advertising has been around for eight decades. Comparatively, FAST CTV and Programmatic is in its infancy.

Typically, programmatic ad exchanges primary advantages are:

1) Ease of use

2) Flexibility (start/stop ad spend on a dime)

3) Highly scalable

The aforementioned advantages are primarily for “brand” or top of funnel marketing. Programmatic CTV also enables opportunities in performance marketing. For example, platforms like Roku are expanding their interactive ad inventory and using highly targeted audience cohorts to drive sales or other conversion (e.g. app downloads) for its advertisers. This “bottom of funnel” performance marketing significantly expands the TAM of CTV (Brand + Performance) versus traditional linear TV (only Brand).

“’Programmatic advertising brings data into the ad buying equation and makes the process both automated and programmable through algorithms and software platforms.”

-WPromote Blog

Mind the Gap - Programmatic Will Close the Gap Between CTV Consumption and Ad Spend

Television advertising budgets are increasingly being caught between a rock and a hard place. At a 30,000 foot view, advertisers must choose between staying the course with linear TV advertising and losing more core audience reach (younger viewers) each year, be less efficient on advertising spend and not embrace the future; or, jump into CTV which offers better returns but more uncertainty, headaches and complexity.

“60% of advertising execs [buy CTV advertising] without knowing the reach, frequency and effectiveness of their campaign.”

- Danielle DeLauro – EVP, VAB

The complexities of buying CTV advertising have significantly held back spending. CTV households make up 60% of the US, while CTV budgets lag and comprise only 16% of TV spend annually!

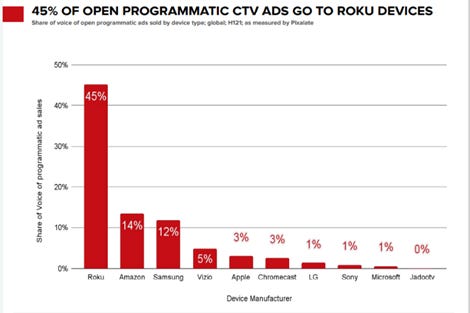

Roku Dominates Programmatic CTV Advertising

Now we are finally ready to get into the meat of the differentiation of the Roku platform. Roku dominates Open Programmatic marketplaces. In the past, it has taken between 45%-69% market share since 2019.

Roku has done a great job in penetrating the dominate advertising spenders in the U.S. About 9 in 10 of AdAge 100 brands have advertised with Roku. This is a solid footprint to build upon as asking for additional budget is an easier sales process than getting/scaling pilot programs.

What are the Bottlenecks Holding Back CTV and Why Does Roku Dominate?

CTV AdTech in is an order of magnitude more complex than linear TV AdTech because it is run by data and algorithms, not humans. Like any new supply chain, there are problems and technical bottlenecks to be worked through.

“CTV and OTT advertising inventory runs the gamut in terms of platforms and industries. The traditional media world has a relatively consistent set of rules, but if you want to break into CTV, you need to be ready to play in the Wild West. From content aggregators to streaming services to smart TV manufacturers, you’ll encounter new rules and priorities at every stage of the way. Even one small technical change can wreak havoc for a marketer’s already limited resources.”

-Demandlocal

Here is a list of potential problems that Programmatic supply chains cause at each segment:

Below was a survey conducted by Digiday of 100 marketers about the main obstacles they face when allocating more budget to CTV spend:

Roku offers arguably the best current solutions to the Programmatic CTV issues listed in the above survey. Roku has three primary categories of advantages to utilize in overcoming these concerns, let’s explore each:

1) Superior AdTech Stack

Solves: Inconsistent Measurement, Frequency

On Measurement:

In today’s advertising market, if ad spending can’t be measured then it won’t scale. CTV advertisers are having a hard time measuring what effect they have on audiences – they are even having a hard time knowing where their inventory is being placed!

In fact, Nielsen, the gold plate measurement brand in advertising and TV lost its accreditation last year due to some technical issues in measurement.

Roku’s primary advantages in Measurement:

RIDA (Roku ID for advertisers) – This is First Party (“1P”) data that enables audience targeting. RIDA uses its logged-in data to build identity. It also allows channel partners, such as programmers, to use its API to access the RIDA

Incremental and guaranteed audience reach - so advertisers can hit untargeted cohorts

Incremental reach guarantees - only pay for impressions that were not duplicated by linear)

Twenty 3rd party measurement partners

Deep, value added partnerships with the marquee measurement service providers such as Nielsen:

“Roku has enabled publishers to measure channel content on Roku devices within Nielsen Digital Content Ratings (DCR). Digital Content Ratings provides access to deduplicated reach and demographic insights for channels on Roku devices to identify which programs most effectively reach key audiences. This increase in coverage helps content owners and advertisers navigate the expanding world of TV streaming and is a major milestone on the path to Nielsen ONE, Nielsen’s transformative, cross-media solution that will enable advertisers and publishers to transact using a single metric across linear and digital television.“

-Roku Press Release, March 2021

On Frequency:

In addition to Measurement, having an AdTech platform that manages Ad Frequency is also paramount for advertisers, consumers and AdTech platforms.

“One of the reasons measurement is so important, …is one of my worst fears is that I know my audience really well and target them and then bombard them with ads”

- Melissa Grady Dias – Global Chief Marketing Officer, Cadillac

Roku’s AdTech stack provides for de-duplication of ads in CTV apps which it started implementing in 2019.

“One of the biggest developments came when Roku acquired Nielsen’s Advanced Video Advertising business earlier this year, giving the company access to Nielsen’s ACR and dynamic ad insertion capabilities. Nielsen had previously licensed its ACR data, including to Roku. But that ACR data is now exclusive to Roku.”

Some of Roku’s competitors have followed suit in using similar technology to de-duplicate advertising. LG, Samsung, and most recently, (late to the party) Google have implemented Automated Content Recognition (“ACR”). That said, not every Smart TV has ACR and it takes time to build/scale this technology.

2) Direct relationship with consumers (1P Data)

Solves: Targeting the Right Audiences

Having a large 1P data pool / customer relationships are critical building block infrastructure in Programmatic.

"We're seeing a lot of interest in that data-driven aspect, whether that be advertisers bringing on their CRM data or other unique first party audiences. The use of audiences is really helping reduce advertising budget waste, and ensure they're reaching who they're intending."

- Kristen Williams, senior vice president of strategic partnerships at Magnite

Roku has already made some inroads in partnering with Kroger and Shopify to build unique advertising supply chains that are more efficient at targeting.

Consider the Kroger partnership; Kroger’s CRM and shopper data is anonymously combined (hashed) with Roku’s 1P data. This enables targeting audiences at a very granular level where Kroger can now specifically run an ad for known ice cream or pretzel eaters instead of spraying and praying an audience cohort with unknown dietary habits. This increases ad spend and efficiency significantly.

“The [Kroger] deal was big because you're getting shopper data. So they get data, we get data and then we're able to go to the CPG firms and say, "Listen, anybody that's on a Roku and they talk about 50 million active users…we know their shopping behavior. So if you're a CPG brand and you can advertise on us, we can actually tell you whether you're getting brand lift or not, which is the holy grail of advertising.”

-Former VP, Roku

3) Reach / Inventory Fragmentation

Roku has over 56.4M active accounts or roughly 30% of the streaming market. Some of these households are ONLY reachable on TV through Roku devices. This cohort of Cord Cutters / Cord Nevers are younger, and comparatively higher impact audiences to target with advertising. This makes Roku an advertising toll booth for ad intensive sectors like CPG that cannot afford to miss these cohorts. Conversely, viewer degradation is becoming a problem for linear advertisers as their most important cohort is no longer on traditional TV.

Roku can offer something truly unique to advertisers. It can offer exclusive, high value audiences and guaranteed incremental reach.

Now, factor in that linear advertising rates have gone up double digits for the past few years and you can see the pressure building on advertisers to spend more efficiently and accelerate CTV efforts.

Where Does Roku Have Room for Improvement?

Ad Fraud:

Fraud is still a major problem in CTV. Up to 20% of traffic is invalid or fraudulent. Roku is not immune to fraud and has failed to prevent a few high profile attacks. That said, Roku will improve on its level of fraud given that direct ad insertion with known sellers and direct programmatic relationships is on the rise. Also, consider how fast CTV is taking share with a high-level of fraud, this means that long-term ROAS is actually more competitive as fraud is eliminated and this will trigger even more future market share gains.

Brand Safety:

The vast majority of Roku’s advertising inventory is brand safe given the content is sourced from major streaming or media companies, though Roku is not perfect.

CTV Ads are Getting More Complex; T-Commerce Optionality

It is important to note that the complexities of the CTV AdTech supply chain are increasing substantially. Compared to linear, ad formats are much more diverse (different lengths, formats, coded with technology and often mapped/paired with audience targeting data).

But more importantly, CTV Ad Exchanges like Roku’s OneView are starting to innovate on top of their AdTech stacks:

1) Dynamic Ad Insertion:

Roku is building the capability to better customize ad delivery through its Dynamic Ad Insertion or DAI. It is doing this through its strategic alliance with Nielsen.

This means that advertisers can more explicitly target households with different products. So if Household A has a dog and Household B has a cat, each can get a Kroger advertisement for the correct pet food instead of wasting a cat food ad on a dog household or vice versa.

2) Interactive ads

Advertisers want inventory that users can pause, click on or interact with

1) Sponsored Content

During March Madness last year, Roku and Turbo Tax partnered to provide Roku users sponsored content and unique ad inventory units. Roku viewers got access to live games, as well as augmented editorial comments and interactivity with VR/AR snapchat lenses.

2) Advanced Audience Cohort Targeting

Some advertisers are able to target audiences with special data protections. For instance pharma companies may require HIPAA-compliant data and targeting capabilities

As the industry moves towards this highly customized and sophisticated advertising, Roku is better positioned to move fast and capture market share. The higher the degree of customization in AdTech, the fewer the advantages of being a large, incumbent AdTech platform such as Amazon and Google aka the Innovator’s Dilemma.

Finally, the holy grail of CTV AdTech is to marry advertising to E-Commerce. This is called T-Commerce. Roku has laid some foundational work with Shopify and Kroger partnerships (mentioned above) to begin executing outcome-based data / performance marketing. While the TV is not a traditional platform or conduit for shopping, even taking a small share of E-Commerce volumes would create a step-change impact in the value of CTV advertising – I am not going to cover this topic in-depth here, it is probably worth its own writeup.

"I think we're going to see a lot more interactivity capabilities, shoppable content and some really unique ad units continuing to come into play in the marketplace,"

-Allison Clarke, head of client development at Vizio.

Sources of Roku’s Future Revenues

The CTV market is so big, and growing so fast, that the market dynamics are much less Roku Vs. Amazon or Google, but more about taking share from the following three sources:

1) Linear TV Budgets are still much larger than CTV budgets

As the chart below highlights, we are still in the very early innings of converting linear TV to streaming.

2) Digital

Roku is not limited to winning advertising budgets directly from linear wallets. Roku’s OneView platform is cementing itself within advertiser’s omnichannel strategies.

As these campaign strategies gain traction, particularly in a post-ATT/IDFA and Cookie tracking world, Roku is well positioned to win share from the broader digital advertising market.

3) Cutting Out the Middleman (Trade Desk and Other 3rd Party Ad Exchanges)

In the previous few years, Roku has had to work with a number of 3rd party Ad Exchanges/DSP competitors, namely the Trade Desk. There are a number of reasons for this, such as audience fragmentation: Ad inventory, especially when audience targeting is layered on, has previously been challenging to fill. However, as Roku’s user base increases and FAST viewership rises on Roku’s platform, it can fill more of its own ad inventory without 3rd party ad exchanges.

But What About the Competition?

I believe that the previously mentioned sources of market share gains are strong enough to propel Roku’s free cash flow into at least a few billion dollars long-term even if Roku loses its dominant position in CTV ads. Importantly, Roku doesn’t even need to remain the top CTV advertiser long-term to hit my targets. I am assuming that Roku’s incremental market share halves from 50% currently to 25% over the next three years:

The last sections ONLY available in the PDF due to Substack memory limits…