Roku Finale: 20%-50% IRRs

Part III of III

Can Roku’s Programmatic FCF Underwrite a De-Risking Pivot?

If Roku can start its content flywheel (chart above), and execute a business model pivot (chart below), and then I believe Roku will cement its long-term competitive fit in the marketplace as a top tier CTV OS Platform + Streaming Content Supplement

Roku still has a strong lead in TV OS hardware, however this advantage will continue to erode. Roku cannot compete against better capitalized Megacap companies like Amazon and Google if its business model stays static. Executing the pivot above is risky and challenging, but the quality of Roku’s moat would improve dramatically.

Roku 2.0 would offer (content hungry and price sensitive) consumers something highly differentiated and its value proposition is not easily copied, even by formidable competition. This would re-rate the stock as Roku’s customer lifetime value would go up (see valuation section below) and its primary terminal value risks (discussed below) would alleviate, which are currently depressing Roku’s stock price.

How Roku Will Win the Battle for the Living Room (and NOT the Streaming War!)

Importantly, Roku is not competing with pure streaming content players with this pivot. It is NOT trying to be Netflix. It is NOT going to be a major player in the Streaming Wars. Roku is trying to win a different war – The Battle for the Living Room.

The Battle for the Living Room is about leveraging the two-way relationship between the CTV viewer and TV OS platform to build a better UX, offer better content and to eliminate the frictions in consuming CTV content. I believe the following are some of the more important long-term product advantages:

Unique Content Access - free content, exclusive original content and/or sponsored content

Roku is aiming to produce 50 original shows over the next two years. This is an ambitious plan but that level of content delivered for free on Roku is an extremely compelling value proposition for consumers. Other notable content highlights include:

a. Quibi

Lower Ad Disruption – Roku ad loads are 7-8 minutes per hour or roughly half of linear TV and it is one of the few platforms that moderates ad frequency (showing the same advertisement over and over which damages viewership/UX)

Discovery – Roku new, relevant and sometimes niche content; content can be unbundled from apps

A major pain point to solve is surfacing on target content for each user to watch without them having to endlessly scroll through different apps and channels.

Removing Frictions to Content Access: Roku users can find/signup/access hundreds of streaming apps with a few clicks

Linking TV to Shopping experiences (detailed in Part II)

So why do the strategies listed above to win the Battle for the Living Room matter?…They lower terminal value risks (higher valuation)

Terminal Value Risk #1: Can Roku Re-Accelerate MAUs?

If Roku can execute the product enhancements listed above then I believe that it can capture market share from any competitor. Roku’s pivot will offer a compelling value proposition to content hungry CTV consumers:

A recurring pipeline of free content for a one-time cost (buying a Roku TV or stick).

Can Roku win over consumer mindshare as a Streaming Content Supplement?

My bet is yes. The 50 original shows over the next two years, 10,000 title library and future $2bn in FCF to redeploy into content (see Part I or II) is likely to generate some level of hits and buzz.

If Roku can enhance its content value proposition enough, it may even be able to coexist among other TV OS systems. That is, why wouldn’t Amazon Fire TV owners buy a Roku stick if the Streaming Content Supplement value proposition is strong enough in a few years? I am not fully underwriting this potentiality in my model, just highlighting that future OS sales might not be a zero sum game.

If Roku’s Streaming Content Supplement strategy works, it would re-accelerate Monthly Active Users (“MAUs”) growth. MAU growth expectations have come in substantially, in my view. If Roku can continue to gather eyeballs in the living room then the rest will work itself out.

Terminal Value Risk #2: Can Roku “De-Risk” Its Content Supply Chain

This is one of the primary long-term bear cases on Roku:v

The theory is that the top streaming apps will scale and spend so much on content that they will push out smaller media companies with inferior content spending. If viewers consolidate in a small number of large streaming apps, this decreases the amount of value that Roku can capture as a distributor of content.

This is known as Wholesale Transfer Pricing Power (“WTPP”) risk

While this risk is real, I simply don’t believe it to be true long-term. I think consumers want a diversity of personalized content and I would highlight the following counter data points:

The Roku Channel now has over 200 licensed content partners and it is growing at double the rate of the rest of Roku’s platform

Creating and owning more Roku Original content (as outlined above) will alleviate WTPP risk

Can Roku “Unbundle” Streaming Content from their Apps?

Roku devices enable a huge opportunity. When a viewer turns on a CTV with a Roku device, Roku controls the “Home Screen” and has an opportunity to deliver content and suggestions.

If Roku can control/drive viewership through its suggestions on its home screen, then this improves its bargaining power with streaming content owners.

Both Roku and Google are prioritizing becoming the home screen and the “search” function for content:

“New to Android TV is the Discover tab that features personalized recommendations based on what users watch and what’s trending on Google. The Discover tab features movie, show and live TV recommendations from across most apps and subscriptions.”

At some point, content could become “unbundled” from specific content apps such as Netflix. However, it is more likely that content from lesser-known Free-Ad-Supported-TV (“FAST”) apps such as Tubi or Pluto TV who exert less bargaining power with Roku. FAST apps are likely be more receptive to unbundling because they monetize their content libraries with advertising.

More viewing hours = more money.

Monetization depends on maximizing content library consumption with FAST models, so this kind of content is more likely to be distributed more broadly with partners like Roku.

Roku’s Valuation – Skyrocketing Economics per User

Roku has a range of ad splits with its content partners. At the high end, it has 100% take rate on advertising inventory that it owns, while it splits revenues 50/50 with its smaller content partners. Larger content partners are believed to share between 20%-30% depending on how much content is licensed to The Roku Channel. Disney is at the bottom end of monetization as it is believed that Roku only splits 10% of revenues for one-time signups of new customers on its app (according to Morningstar).

In other words, Roku’s incentive to drive viewership to independent apps is incredibly strong.

On a recent expert interview, a Vice President of one of the leading programmatic verification platforms estimated that The Roku Channel comprised approximately 15% of all Roku’s programmatic advertising platform. Historically, the perception was that The Roku Channel only offered junk library content that nobody watched, so getting this level of viewership is a solid sign that Roku’s content pivot is getting traction.

If Roku can continue to migrate users to these lesser-known apps and content pools, then not only will its FCF inflect from higher ad splits, but it will also alleviate a lot of pressure in negotiating with larger content suppliers given Roku will be less reliant on them.

Summing it All Up

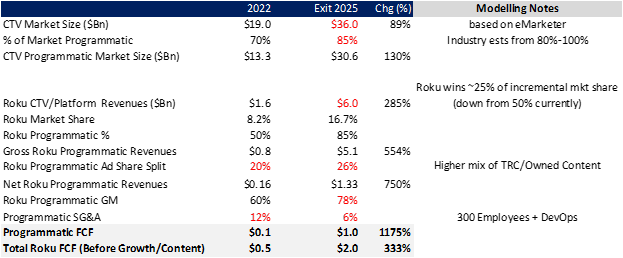

The chart below is the Roku thesis’ North Star. The assumptions were pieced together through a smattering of financial reports, industry interviews and forecasts as well as expert calls with former Roku employees. Any one assumption has some variability but I attempted to be conservative. I actually believe that the overall CTV forecasts are conservative because:

1) Historically the CTV ad growth has outpaced forecasts and;

2) Programmatic infrastructure is finally getting to the point where it can accelerate marketing budget wins from linear (discussed in previous Part II section)

I believe that Roku can generate $1bn in FCF from programmatic alone, which would put total Roku exit 2025E FCF closer to $2bn BEFORE content and growth spending. This does not compare apples-apples with the Street FCF of $1.2bn in 2025E, but I am directionally higher by a fair amount.

I am not fixated on mapping to Street consensus, but rather, my bull view on Roku is can get to a comfortable point in FCF generation where, if needed, they would have the option to invest up to $2bn in original content.

The Bottom Line: Inflection in user-centric valuation implies 20%-50% IRRs

There are a ton of different approaches to Roku’s valuation. One of my primary guideposts is the user-centric valuation approach below. There are some key assumptions, namely:

1) Revenue Growth - accelerate from higher ARPU (low execution risk), even with conservative MAU growth assumptions.

2) Platform Gross Margins - inflect from higher incremental margins as revenue mix shifts to automated programmatic exchanges

3) Churn – lower moderately as product-market fit improves

Market has a Dispersed View on Roku’s Valuation

Historically, Roku has been an extremely violent stock. Investors have struggled with what to pay. NTM revenue multiples have ranged from 4x to 26x and on an LTM EV/GP basis multiples have ranged from 40x to 185x. A lot of this variance is related to natural market fluctuations and the fact that Roku is still an early stage, unprofitable business for its entire existence in public markets.

However, the largest driver of Roku’s valuation volatility, in my view, is the market (over)-reacting to the terminal risks outlined in this writeup e.g. OS market share threats from AMZN, GOOG and sourcing content/WTTP Risk.

Therein lies the core of this thesis. If we have confidence that Roku can scale to several billion of FCF to fund content, then it will cement itself as a toll booth in streaming that can’t be elbowed out of the CTV value chain.

Inflecting unit economics + De-risking business model = multibagger

Thank you for reading!

-A Man in A Basement

Thanks for the writeup. It seems that Roku would be a great company as a toll booth, but not if it has to keep spending on content to keep itself there, to de-risk its business, and to grow users. Imo, spending on content does not build a cumulative competitive advantage (most content is not evergreen). In other words, Roku will not be able to one day stop the content spend and be confident that it will keep its competitive position. The terminal economics might not be so great considering the cashflows that need to be reinvested. Curious about your thoughts.

Ironically, when I wrote the linked article on WTPP, I was envisioning ROKU as the perfect example of a company using WTPP as an advantage. My theory was that if you're a big streaming company like Netflix, HBO, etc you have to map every step of the way from creating/licensing content to delivering it to consumers on a screen. Then each step along the way you have to analyze what is the negotiating power of the input.

We've seen with Netflix that at first they had to shell out money to license shows in order to attract and keep subscribers from churning, but now they're able to spend almost purely on original content. However, how about other steps along the chain, like physically getting content in front of viewers? They're (likely) not going to vertically integrate and create their own devices, so instead they're reliant on a distributor to provide the Netflix app. That's where ROKU thrives, and that's what provided ROKU with all the leverage when negotiating with HBO: https://www.theverge.com/2020/12/16/21272058/hbo-max-roku-watch-wonder-woman-1984-movies-amazon-fire-stream-comcast-warnermedia

Would love to hear your thoughts, and you've got a new subscriber in me. Looking forward to reading more of your work.