Digital Turbine Part I - Sketchy Past, Bright Future?

4th post of the 500 hour project

500 Hours Update:

I began writing on Substack primarily just to build a better professional network. So far, it has worked out incredibly well and I have even been fortunate enough to land a handful of sub-advisory contracts in which I lend out some spare analytical capacity on a single stock, sector or special project. If this interests you, please feel free to reach out directly at stockdweller@gmail.com

These contracts have also been responsible for the delay in writing up my next stock idea, but now that I have some time/freedom back, I am going to writeup Digital Turbine (NASDAQ: APPS) in a two-part series.

Overview of next write-up: Digital Turbine (NASDAQ: APPS)

Digital Turbine has a lot of hair on it at first glance: super shady listing process and underwriters, a borderline Going Concern notice and a Wells Notice not that long ago, leverage (>3x), a frenzy of M&A that pollutes accounting, and a checkered track record of management execution - whew!

With all that said, in Part I (below) I will highlight why I think DT has turned a corner from its spotty history and explore the power of DT’s core technology platform - Ignite. Part II will focus more on understanding how its recent, large acquisitions fit together to create a formidable AdTech platform as well as potential synergies – this is where the money will be made (or not)!

The bottom line is that I think DT has asymmetric upside potential between 3x and 7x if it executes on its AdTech platform, while downside risk is protected from a (relatively) modest valuation (for software / AdTech ofc!) with a forward sales multiple >40% below the average Russell software company. FCF conversion is also high and $APPS is FCF positive.

Recommended reading before this article

1) Two years of transcripts

Part I) Emerging from the Shadows with Unique Assets and Enhanced Governance

Digital Turbine has a scrappy background. It is a collection of ~10 acquired properties – though roughly half of these are either too small or irrelevant to matter at present. In 2014, Mandalay Digital bought a company called Appia, executed a reverse merger and changed the name to Digital Turbine. It then raised a series of small and expensive pieces of hybrid / equity capital with its largest offering underwritten by a scam-ridden investment bank Ladenburg Thalmann & Co.

In addition, DT’s management team had a fairly checkered track record of execution in managing a public company. Multiple years (2014-2018) of consecutive internal control issues led to a Wells Notice. There were also some pretty aggressive short seller reports which are worth a read. I actually think most of the short seller’s arguments were likely accurate at the time. That said, the worst parts of the thesis are no longer relevant (predatory investors), however, I am not completely sold on the CEO/management yet (will address later in Part II).

In sum, Digital Turbine’s origins were sketchy. For me, these are all enough reasons to pass by themselves, let alone together.

Then, the story gets stranger…

In 2017, Digital Turbine was able to secure a $5M credit facility with Western Alliance Bank. Three years later DT then secured a $100M with a top tier Wall Street syndicate and then this facility was quickly increased to $400M! Digital Turbine used the proceeds from these banks to go on an acquisition bender. It subsequently acquired 4 companies for >$1 billion – though keep in mind earnouts make up a large chunk of the price (I will cover these assets in detail in Part II).

It is really, really strange to see a company with a checkered past 100x their revolver capacity (without raising support capital) using legitimate banks in such a short period! Just to reiterate, this is bank capital – there are regulators (OCC) governing this kind of lending.

The key question I asked myself: what is it that these bankers saw to give them comfort / collateral? It is a strange setup to see bank debt step-in, when hybrid/equity capital markets passed!

I am someone that likes to view tech through a credit lens from time to time. I think the graduation to looser covenants and speed/magnitude of the revolver capacity increases says something interesting about the risk profile of DT’s cash flows. DT must have a stable base of durable cash flows that bankers can use to justify to regulators the amount of dry powder that they just lent to let a relatively unknown, unproven and questionable management team.

Stability from Telco/OEM contracts with Rational Duopoly/Oligopoly characteristics

One of the reasons why I believe Digital Turbine was able to access a high-caliber revolver and use it to LBO a bunch of AdTech assets is because of their inherent position as the globally dominant pre-installed app company. Digital Turbine’s core Ignite platform successfully executed some tough but lucrative TelCo/OEM contracts. These TelCo/OEM relationships often take 5-8 years to cultivate and require heavy IP buildout for different regions and phone capabilities.

The Pre-installed niche is a winner-take-most scale game. Users from OEMs and TelCos must be aggregated together in order to capture efficiencies for app publishers/advertising partners.

More users/devices → greater ad efficiency → more TelCo revenue splits → more devices

DT has a monthly reach of 1.5bn which puts it near the top of any global user or adtech platform - not bad for a $5bn market cap company:

Once a device is sold with Digital Turbine’s ignite software, DT can then predictably monetize app installs. Android users typically download 8-12 app downloads per device and Ignite gets paid roughly 30c-50c per install in North America (international is much less).

As the chart below highlights, predictability of cash flows was solid even in the earlier days (chart is from 2018) of Ignite/TeleCo relationships:

So given the predictability of cash flows and quality of counterparties (e.g. Samsung), it is a little easier to see how DT got such a large leash from bankers (as well as lots of potential future deal fees ofc!).

Now that I have beat to death the outsourced due diligence / improved corporate governance through debt investment angle, I want to talk about why I think DT’s core Ignite business is set to continue inflecting.

Bullish on the app “real estate” of Android Devices

I find it helpful to view the Android device as a mall and DT/Ignite as the mall operator. DT will maximize revenues by:

1) Manage the largest number of malls (devices)

2) Fill the malls (devices) with as many high-quality tenants (apps) as possible.

DT has done a great job of acquiring malls (devices):

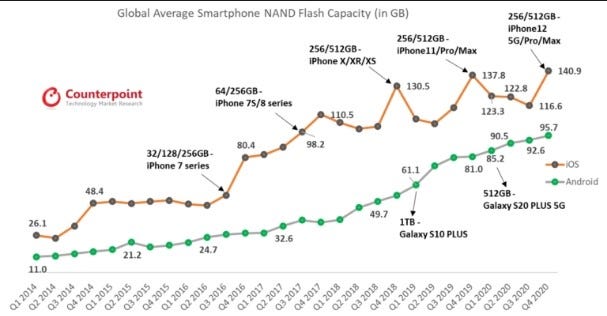

Additionally, the size/capacity of these malls (devices) have gotten bigger…

The monetizable space of a mall (device) is governed predominately by two things:

1) Memory of the device

2) User’s willingness to download apps

Both of these are naturally trending higher which means more revenue per device potential for DT.

Phone memory capacity has steadily increased over time. Memory is still a bottleneck in older/international model phones.

User’s willingness to download more apps has also been increasing:

The chart above highlights consumer’s willingness to download about a dozen apps – but think about the latest push by brands to go direct to consumer. There are over 22,000 direct to consumer brands in existence according to Bluecart. Add in some competition from the labels in the chart below and you can see that the number of tenants (apps) who want to get on devices are growing much faster than the supply of app real estate (slots) on user’s phones.

I think that this leads to strong pricing power for DT as apps compete for limited space/attention on devices.

Looking out into the future, it is hard to see how people won’t use mobile apps more often. The value to brands of having an app / mobile relationship with their users, particularly super users, seems to be increasing demonstrably:

Nike Brand Manager: “[Apps] are super important. It is product…treat it as a product investment to really soup up the data layer that you have around your customers and find ways of promotions, giveaways, whatever the heck you need to do to really start to engage with them, get them to download the app. And engage with them that way.”

DT Gets No Credit for De-Risking

In Part II, I will cover the nitty gritty valuation of DT as well as the sexiest part– the synergies of its AdTech platform.

However, for this last section and before we go into depth on valuation/AdTech, I want you to consider the progress on DT’s core platform in isolation…

Sustained very strong double digit organic growth rates but step changed from ‘millions’ to ‘billions’ in revenue

Recurring revenues going from 10% to >50%

Customer concentration from >50% to <15%

Cost of debt capital re-rate from mid-teens to low single digits (revolver)

Arguably, any company that undergoes this kind of transformation should re-rate substantially higher. However, as the chart below highlights, valuation has fallen back down into historical ranges:

One way to interpret the mean reversion of the multiples above is that the recent M&A spree of AdTech companies is roughly offsetting the de-risking milestones listed above.

In Part II, I will breakdown the real secret sauce of DT and why I think the AdTech properties that DT acquired, when stacked onto Ignite, position Digital Turbine for substantial revenue growth, margin expansion and valuation re-rate.

Thank you for reading!